The Madrid City Council’s Economic-Administrative Court clarifies criteria regarding the Municipal Capital Gains. And this before a claim that we present from our Legal Consulting Dept, for the amount of 33,607€ paid by our client for the concept of Tax on the Increase in Value of Urban Land. The one known by all as the Municipal Capital Gains.

We will summarize below the foundations of the City Council, which leaves fixed the bases to determine the origin or not of the Municipal Capital Gains.

The Municipal Capital Gains

First of all, and as background, it is worth recalling the criteria of the Sentence of the Constitutional Court 59/2017, and the interpretation made by the Supreme Court of this sentence and that we already commented in two notes.

In summary, that judgment stated as follows:

- Article 110.4 of the Local Treasury Law is unconstitutional because it prevents taxpayers from proving the non-existence of an increase in the value of land.

- On the other hand, articles 107.1 2 of the same legal text are fully constitutional and therefore applicable. In those cases in which there is an increase in the value of the land, which is evidenced as a consequence of a transfer.

- In the absence of a legal norm that establishes how to determine whether or not there has been an increase in the value of the land, it falls to the taxpayers to demonstrate by any means admitted in Law, the non-existence of an increase in the value of the land that makes the payment of the municipal capital gain inappropriate.

- The taxpayer, who has the burden of proving that there has been no increase in the value of the land on the date on which the tax accrues, may prove this:

- for the difference between the purchase price and the sale price reflected in the public deeds.

- by expert evidence, carried out by qualified professionals or by companies or valuation entities approved by the Bank of Spain. Provided that they contain specific and well-founded valuations on the spot.

- any other means of proof, such as, for example, a tax verification of the values declared either as a result of acquisition or disposal, carried out by an Administration other than the City Council (i.e. AEAT or Autonomous Community).

Municipal Capital Gains in Madrid

Having said this, the Madrid City Council argues in its Resolution that in order to determine whether there has been an increase or decrease in the value of the land, one cannot simply resort to the concept of capital gain or loss determined in Personal Income Tax or Corporate Tax. In such a way that elements such as the taxes levied on the operation, improvements or financing costs cannot be brought up to determine whether or not there has been an increase in the value of the land, because they are not directly or indirectly related to the objective determination of the value of the land.

Criterion of the Tribunal

It is therefore a question of determining whether in the acquisition and disposal of a given property, built on urban land, has experienced an increase or decrease in the value of the land. And for it, it will be necessary to resort to the value of transmission, but since the same one refers to the whole building and not only to the one of the ground, it will be necessary to dissociate the part of that total value that corresponds to the ground and the part that corresponds to the value of the constructed thing in it.

Being reasonable to resort to the cadastral information of the property that specifically determines the value of the land and construction. In such a way that applying this proportional relation to the total of the property, the value of the land can be established as much in the previous date of the acquisition as in the date of transmission. It is reasonable to resort to cadastral valuations that are based on exhaustive technical studies that serve for the assignment of the cadastral values of the properties, and that are also issued by a different administration to the town councils that are the ones that liquidate the municipal capital gains, and therefore are more objective and impartial.

And in the event that several properties are transferred in the same public document under the same legal transaction or for the same title, without individualising the amount corresponding to each of them, the same proportionality criterion should be applied as described above.

Variables to be taken into account

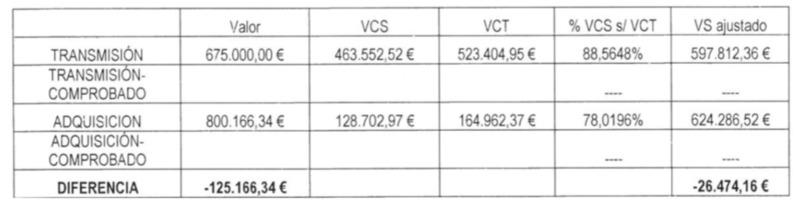

Therefore, when a property is transferred, and to determine whether there is an increase or decrease in land value, the City Council will take into account the following variables:

- Value = amount that appears in the public deeds (both those of acquisition and those of sale)

- Land Cadastral Value (LCCV) = both on the dates of transmission and acquisition

- Total cadastral value (TVC) = also for dates of acquisition as transmission

- Percentage of the VCS over VCT = percentage that represents the value of the land over the total value.

- Value Adjusted Land (VS) = value of the adjusted land, applying the previous % on both the date of transfer and the date of acquisition.

The calculations made by the City Council in the case of our client, applying the above factors, and for which it concludes that there is no increase in value, are detailed below, as they are very clarifying:

It is therefore clear that the criteria followed by Madrid City Council to determine whether or not there is an increase in the value of urban land, and consequently, the origin of the payment of the municipal capital gains tax. And given that it is based on the jurisprudential criteria of our highest court, it will also be applicable before other City Councils that claim this tax inappropriately.

If you need our help, do not hesitate to contact us.

Arrabe Integra

Legal Consulting