The Taxation of Digital Content Creators is often a matter of doubts and questions. What is the best formula for a creator if through a society or not.

From our Tax Consulting Department, we try in this note to bring a little light on the matter. Especially for Digital Content Creators, for Youtube, Facebook, Instagram, blogs, etc.

Digital Content Creators with tax residence in Spain can carry out their activity as self-employed professionals. But also through a company set up for this purpose.

Taxation of Digital Content Creators. Alternatives

The tax consequences of one option or the other are very different. So this issue has been in the focus of the Tax Administration for years.

In the case of opting to carry out their activity as self-employed professionals it will be necessary to register in the Special Regime for Self-Employed Workers of the Social Security (RETA). In addition, the economic activity carried out must be registered with the Tax Agency.

While the Courts have interpreted, with nuances, that the obligation to contribute as a self-employed person to the Social Security can be avoided if the income does not exceed the Minimum Interprofessional Salary. However, the obligation to register with the Tax Agency applies from the moment the activity begins. Regardless of the volume of income generated by it.

In this scenario, the creator must issue the corresponding invoices for the income generated. If the entity invoiced is resident in the Spanish mainland or in the Balearic Islands, the invoice must also include the corresponding VAT at the rate of 21%.

However, if the invoice is issued to a foreign or resident company in the Canary Islands, Ceuta or Melilla, no VAT will be charged.

In addition, the creator who carries out his activity as a self-employed professional must declare the income from his activity in his annual personal income tax return. In which he will pay tax on the profits generated by his activity. The profit being the difference between the income obtained and the tax-deductible expenses.

Digital Content Creators. Personal Income Tax (IRPF)

Although the way in which the tax to be paid is calculated is relatively complex and depends on multiple personal and family circumstances, in a simplified form it can be said that the income obtained will form part of the general taxable base of personal income tax, which is taxed according to a double scale:

- on the one hand, the national scale, common to the entire national territory, is applied

- and on the other hand the regional scale approved by each Autonomous Community.

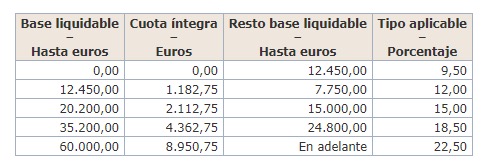

The national scale is as follows:

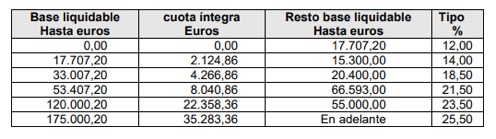

As far as the regional scales are concerned, there are notable differences between Autonomus Communities. For example, the scale applicable for residents in Madrid is as follows:

Meanwhile, in Catalonia the scale of application is as follows:

Therefore, while the CAM will be taxed at rates ranging from 18.5% to 43.5%. But in Catalonia the rates could range from 21.5% to 48%, so the difference is very significant. In both cases, adding the national and regional scales.

In the meantime, if you operate through a company, it will be that company that will invoice the income generated. That for the profits obtained will be taxed at the rate of 25% in the Tax on Corporations. 15% in the first year with profits and the following year, under certain conditions.

Digital Content Creators. Tax Conclusions

However, it should be noted that society itself is not generating the revenue. Rather, it is the creator who produces them with his activity. For this reason, the creator must be remunerated for it, in accordance with tax regulations.

The tax regulations provide that in these cases the partner must invoice his company at least 75% of the profits generated by it. Therefore, a professional activity as a self-employed person must also be registered with the Tax Agency. In addition, if the creator is a director of his own company, he must compulsorily register in the system of self-employed Social Security, with higher contributions.

However, both the Tax Administration and the Courts of Justice have clearly established that when the company is a mere interposed company, with no material or human resources of its own beyond the work of the partner, the latter must invoice his company for 100% of the profit obtained by it. In such a way that the profit of the company would become zero, and the totality of the profit generated by the activity of the creator would be taxed again in his personal income tax return, with the rates explained above.

In short, if everything is done correctly, carrying out the activity through a company would only have added more problems and accounting and administrative obligations, without taxation having really improved.

Arrabe Integra

Tax Consulting