The new contribution basis for domestic employees in 2023 has been published in the BOE of March 31/March 31 in Order PMC/313/2023. This order modifies the previous Order PCM/74/2023, dated 30/January, which developed the Contribution Order for 2023.

Contribution basis in 2023

This update is motivated by the increase in the SMI published in Royal Decree 99/2023 of February 14. And as a consequence of this, the minimum contribution basis must be updated based on the same. As stated in Article 19.2 of the revised text of the LGSS. In general terms, it is affected as follows:

- The Minimum Contribution Basis is set at €1,260.00 per month.

- Fixed-term contracts of less than thirty days will have an additional contribution of 29.74 euros to be paid by the employer at the end of the contract.

- Training and apprenticeship contracts and alternating training contracts. When the monthly contribution basis for common contingencies does not exceed the minimum monthly basis, the contribution will be a single monthly payment of €61.24 for common contingencies. Being €51.06 charged to the employer and €10.18 charged to the employee). And another €7.03 for professional contingencies payable by the employer.

The differences in the liquidations of quotas of the months of January and February 2023 to the Social Security, will be reviewed ex officio, by the administration itself. The administration will notify the deadline in the voluntary period to proceed with the payment of the differences, without additional surcharges.

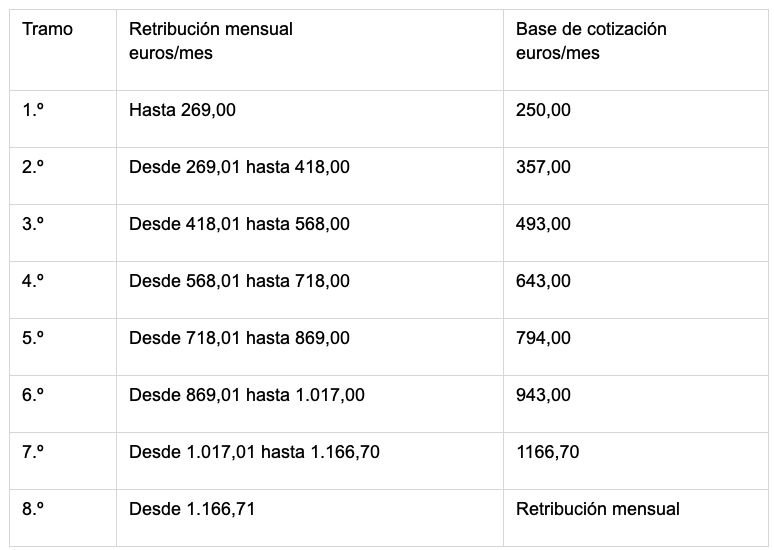

Contribution basis for domestic employees in 2023

With the beginning of the year, the contribution bases for this group have been updated. With the entry into force of the General State Budget, which will be as follows:

Regularization of liquidations of the domestic employees regime

The contributions corresponding to the liquidation period of March 2023, will be calculated applying the new contribution basis foreseen for this fiscal year.

The contributions corresponding to the settlement period of February 2023 will be regularized in the month of May through the issuance of the corresponding complementary settlement. No action is required on the part of the interested parties. Said complementary liquidation will be charged, together with the contributions for the month of April, to the bank account that the interested party has notified to the General Treasury for the payment of Social Security contributions.

The contributions corresponding to the liquidation period of January 2023 will be subject to regularization as from June 2023.

Other changes for 2023

In addition, you should take into account other changes that will occur in the new year.

As from January 1, 2023, it is no longer possible to agree with household employees who perform less than 60 hours of work per month per employer, the assumption by the latter of the obligations in terms of contributions and affiliation and registration with the Social Security, as was possible until now.

Employers who had previously opted for this formula must communicate, before the end of January 2023, to the General Treasury of the Social Security all the data of the employment relationship, bank details, etc. To assume the contribution obligations. To do so, you can use the Import@ss portal.

Changes in bonuses

The bonuses approved with the entry into force of the unemployment and FOGASA contributions are maintained this year. But throughout 2023 there will be changes in some of the existing ones:

- Large families will be able to access, until March 31, 2023, a 45% rebate. In this case, the 20% contribution reduction on the employer’s contribution for common contingencies will not be applicable. However, the 80% rebates on the employer’s contribution for unemployment and the Wage Guarantee Fund will be applicable.

- As from April 1, 2023, a new bonus of 45% or 30% on the employer’s contribution to the social security contribution for common contingencies is established. When they meet the requirements of patrimony and/or income of the family unit or of cohabitation of the employer under the terms and conditions to be established by regulation. This rebate will be an alternative to the 20% reduction of contributions. However, in any case, the 80% rebate on unemployment and Wage Guarantee Fund contributions will be maintained.