Reminder of the new contribution system for Self-Employed in 2023, effective since January 1st. This new contribution system was established for self-employed workers based on the annual income obtained in the exercise of all your economic, business or professional activities.

The contribution base will be chosen according to the forecast of the monthly average of the annual net income according to a general table of bases. This will be fixed each year by the General State Budget Law.

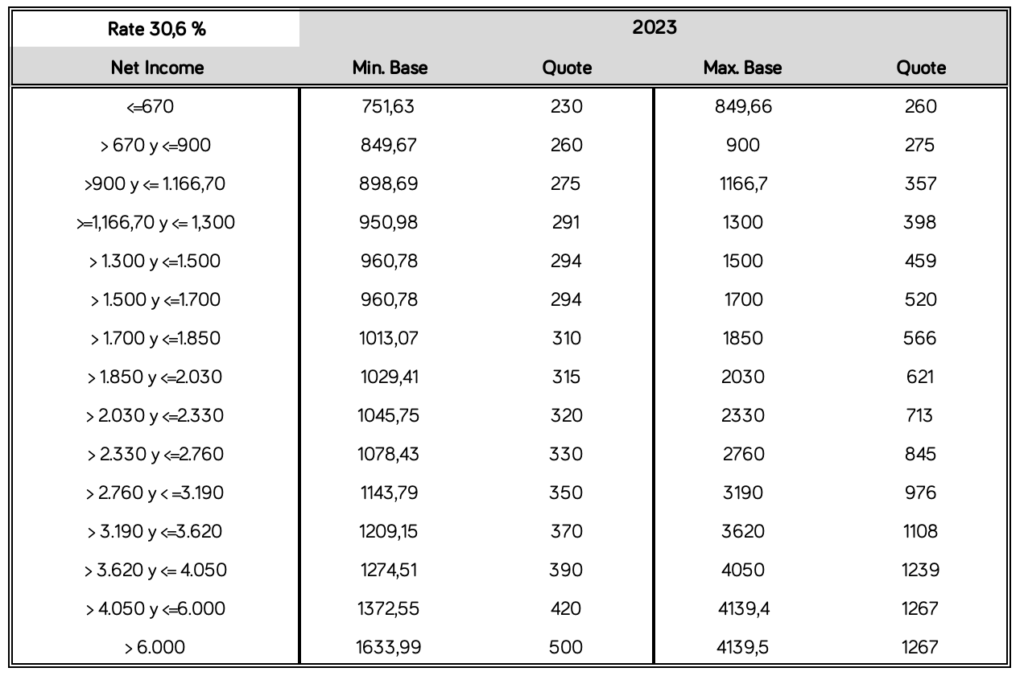

New contribution system for the Self-Employed in 2023

This table establishes a series of consecutive brackets of net annual income, on a monthly average, to which a minimum contribution base and a maximum base are associated.

The bases chosen will be provisional until the time of regularization in the following year. According to the annual income obtained and reported by the corresponding tax authorities.

At the time of applying for registration, the contribution base must be chosen, based on the forecast of the average monthly net annual income. The contribution base chosen will be provisional and will be the same for all situations protected by the Social Security system.

Calculation of the contribution bases for self-employed workers

For the calculation, all the net income obtained from the different activities carried out as a self-employed worker must be taken into account. To which must be added the amount of the Social Security contributions paid if taxed under the direct estimation regime.

The calculation of this net income will be carried out in accordance with the provisions of the Personal Income Tax regulations. And with some specialties in function of belonging to groups as for example mercantile partners.

A deduction for generic expenses of 7% will be applied to this net income. Percentage that, in the case of business partners or labor partners, who have been registered as self-employed for 90 days during the year, the deduction is reduced to 3%.

If you are already registered as self-employed on January 1, 2023, you must report your income before October 31, 2023, through the “Modify your self-employment data” service. Unless a change in the contribution base has to be communicated because the income implies a different contribution base to the one for which you have been contributing.

Change in the contribution base

In the latter case, you must:

- request a change in your contribution base

- and communicate the forecast of annual net income, on a monthly average, before February 28th, in order to avoid having to make any subsequent regularization of contributions.

For the economic, business or professional activities carried out individually by the self-employed worker, the following boxes will be taken as a reference (national declaration) as computable income:

- Economic activities Direct Estimation. –

- Net income + social security contributions or contributions to alternative mutual insurance companies of the holder of the activity. – Boxes 0224+0186

- Economic activities Objective estimation. –

- Previous net income. – Box 1465

- Previous net income from agricultural, forestry and livestock activities Box 1539.

- Income Attribution Regime. – Box 1577

For the economic, business or professional activities carried out as a partner or member of any type of company or entity, in addition to the income that could be obtained from their own economic activity carried out individually, the full income from work or movable capital, in cash or in kind, derived from their condition as partners and/or administrator, as well as the income of said nature obtained in their condition as self-employed worker partner of an associated work cooperative, will be computed.

Income Table for 2023

Superior Bases by previous election

For 2023, if you have a higher contribution base on December 31, 2022 than what would correspond to you, you can maintain that contribution base, or a lower one, even if your income determines a lower contribution base than any of them.

Relatives and Partners

During the year 2023, the family members of a self-employed worker will contribute for their net income. However, if they have been registered in the Special Regime for Self-Employment, as a collaborating family member of a self-employed worker for at least 90 days in the calendar year, the minimum contribution base cannot be less than 1,000 euros/month.

During the year 2023, the partner will contribute for the net income. However, if you have been registered in the Special Regime for Self-Employment, as a partner of a trading company or a labor company, for at least 90 days during the calendar year, the minimum contribution base cannot be less than 1,000 €/month.

Forecast Change of Income during the year. Six base changes are foreseen

If it is foreseen that the annual net income, on a monthly average, is different from that initially foreseen, the contribution base can be adjusted up to six times in the “Modification of self-employment data” service.

For this purpose, a contribution simulator will be available for review and adjustment to the new contribution system. Taking into account the situation of the income at the time of the consultation. The modification of the bases is not immediate, but depending on the time at which the communication is made. So, the change will be effective on the first day of the following months: March, May, July, September, November 2023 and January 2024.

The objective of this service is to make it possible that at the end of the year the result of the regularization is zero.

Regularization of self-employed workers’ contributions

Under the new contribution system, self-employed workers will pay contributions based on the net income obtained from the exercise of economic, business or professional activities. According to the forecast of the annual net income, a monthly average is calculated and a contribution base is chosen within the bracket associated with the amount of such average.

The bases chosen will be provisional until the Social Security General Treasury performs the annual adjustment according to the income reported by the Tax Administration.

If, after the result of the regularization, your annual income is lower than you had expected, the Social Security General Treasury will automatically refund the difference between the contribution you have paid and the one you have to pay. If your final annual income is higher than expected, your situation will have to be regularized by paying the difference.

Cases in which the regularization will not operate

These cases are:

Firstly, registrations presented after the deadline or registrations ex officio due to the action of the Labor and Social Security Inspection. The period between the day you started the activity and the last day of the month in which the registration is requested will not be regularized, if this request is made from the month following the month in which the activity started.

Additionally, when you fail to comply with the obligation to file the Personal Income Tax return.

Also excluded from the regularization are the contributions corresponding to the months taken into account for the calculation of the regulatory base of an economic benefit of the Social Security system recognized prior to the date of the regularization, among other cases.

The contribution bases referring to the periods in which the self-employed worker has received a short-term benefit will not be regularized either. For example, when the self-employed worker is in a situation of temporary disability, birth and care of a child or cessation of activity, among others.

Finally, the period of enjoyment of the flat rate will not be regularized. Even the zero rate for the Self-employed in the Community of Madrid.

Reduced Rate

With the new contribution system, the following benefits are maintained:

- Flat rate of €60/month, recognized prior to January 1, 2023 up to the maximum period of duration. In the case of self-employed workers in the agricultural sector, the flat rate of 50 €/month.

- For the hiring of an employee for the reconciliation of family and professional life of the self-employed worker.

- In situations of leave due to birth, adoption, foster care, fostering, risk during pregnancy and breastfeeding.

- For reincorporation after the birth of a son or daughter, adoption, foster care for the purpose of adoption, foster care and guardianship.

- Family collaborator of the self-employed worker.

- Family member of the owner of the farm.

- Self-employed workers in Ceuta and Melilla.

In addition, some new benefits are included:

- Flat rate of €80/month, recognized after January 1, 2023. Self-employed who have not been registered in the last two years.

- For care of minors affected by cancer or other serious illness.

To enjoy these benefits you will have to be up to date with the Social Security and the Treasury. Check the requirements for each of the assumptions.

If you are currently enjoying the flat rate, in the previous regulation, the same flat rate is maintained, under the same conditions, until the end of its maximum period of duration.